The Copper Squeeze Is Coming

Copper doesn’t get the same breathless headlines as gold, AI stocks, or Bitcoin.

It’s not flashy. It doesn’t inspire doomsday commercials or social media manias.

It just sits there, quietly doing the work. It runs through power lines, motors, transformers, data centers, homes, factories, electric vehicles, defense systems, and the grid itself.

And that’s exactly why copper matters so much right now.

The Copper Squeeze Is Coming

We’re living through one of those strange moments in market history where the world is trying to electrify everything, digitize everything, automate everything, reindustrialize supply chains, build out AI infrastructure, and modernize defense systems all at once.

The problem is that all of those trends lean on the same metal: Copper.

And LOTS of it…

The International Energy Agency says copper is the largest established market among key energy minerals, and even in its base policy scenario, demand keeps climbing meaningfully through 2040.

In its 2025 outlook, the IEA warned that expected mined supply from announced projects still falls about 30% short of projected copper demand in 2035.

That’s not a cute little mismatch. That’s a structural problem.

The World Wants More Copper Than the Industry Is Ready to Deliver

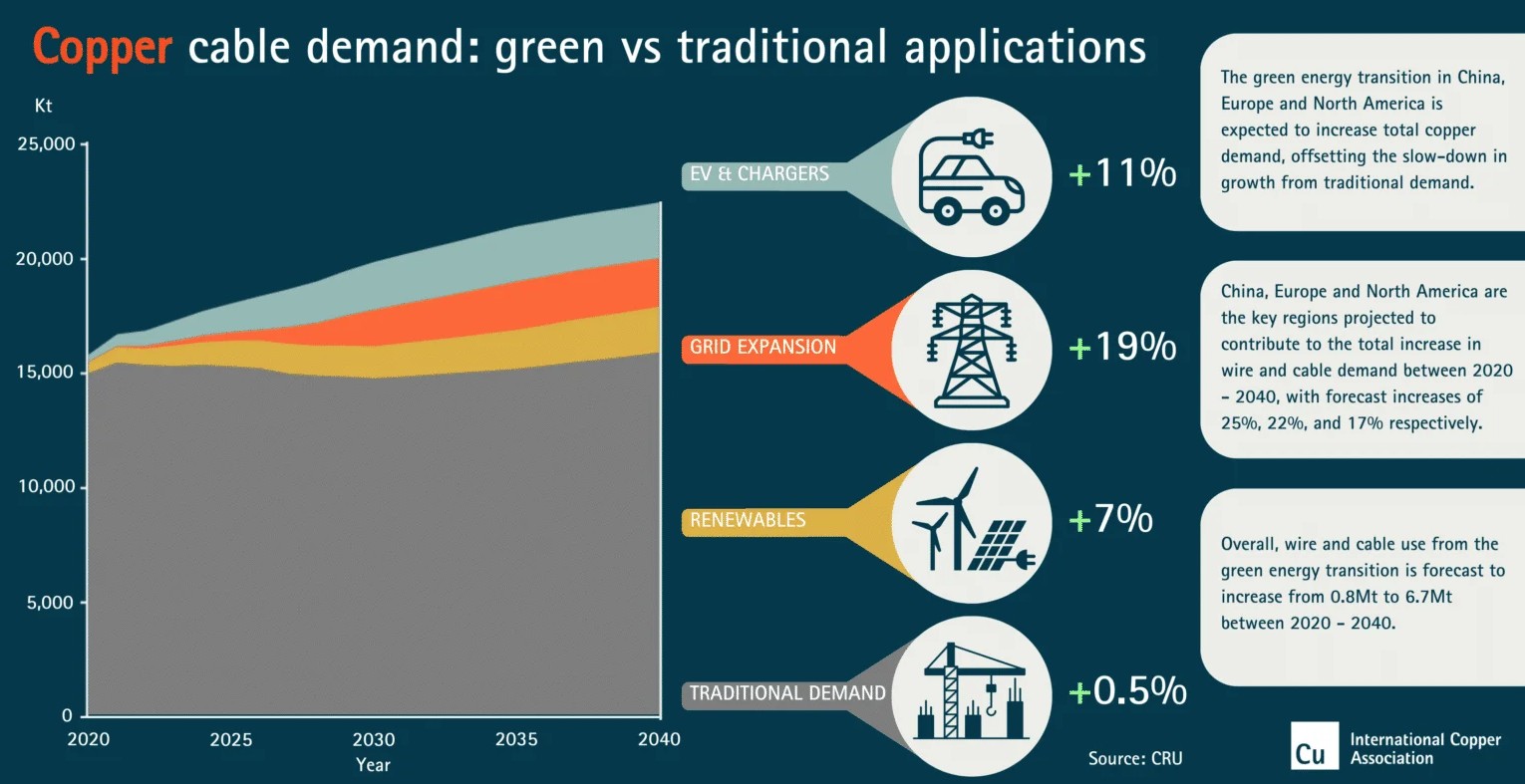

Copper demand is no longer being driven by one theme. And that’s what makes this setup so interesting…

This isn’t just an EV story, and it isn’t just a housing story either…

It’s power generation, power transmission, grid hardening, air conditioning, industrial machinery, military hardware, renewable build-outs, conventional energy infrastructure, and now AI data centers layered on top of all of it.

The IEA’s 2024 analysis projected that copper demand rises by 50% by 2040 in its Net Zero Emissions scenario.

And global mining giant, BHP has projected global copper demand could grow around 70% to more than 50 million tons annually by 2050.

S&P Global, looking through the lens of electrification, digital infrastructure, AI, and defense, recently projected global copper demand could rise about 50% to roughly 42 million metric tons by 2040 from 28.4 million metric tons in 2025.

That demand picture matters because copper doesn’t have a lot of easy substitutes when you need conductivity, durability, and scale.

Yes, there can be some thrift and substitution around the edges. But around the edges is not where the world lives.

The world lives in transformers, cables, motors, substations, and transmission systems. It lives in the physical stuff.

And physical stuff needs physical metal.

The Best Free Investment You’ll Ever Make

Join Gold World today for FREE. Get the latest insight on gold, silver, and precious metals delivered straight to your inbox. When you become a member today, you’ll get our latest free report: “The Dawn of NatGold.” Don’t Delay!

After getting your report, you’ll begin receiving the Gold World e-Letter, delivered to your inbox daily.

The Supply Side Has a Very Different Personality

Here’s where the story gets serious…

When demand rises for software, more servers can be installed. When demand rises for certain consumer goods, factories can add shifts.

But when demand rises for copper, the mining industry can’t just snap its fingers and produce a few million extra tons next quarter.

If you think molasses is slow in the wintertime, then you haven’t seen the supply side of critical minerals…

Only 5% of copper deposits discovered over the last 35 years were found in the last decade.

That’s a stunning statistic.

And fewer major discoveries today means fewer mines tomorrow.

And as if it weren’t bad enough that significant discoveries in the last decade have been limited…

The total resources discovered from 2010–2020 dropped sharply versus the prior decade. So it’s not something that looks like it’s getting better.

This is how shortages are born…

Not in a single dramatic event, but in years of under-discovery, underinvestment, permitting delays, and declining ore quality that eventually collide with a surge in demand.

The market can ignore that mismatch for a while. Then one day it can’t.

Copper Mines Are Not Built on Wall Street Time

One of the biggest reasons copper supply is so stubborn is that it takes forever to bring a mine into production…

Some of the latest research says the average lead time for mines that began operating between 2020 and 2024 reached 17.8 years… Nearly two decades!

A few years ago, earlier work put the average at roughly 16 years from discovery to startup. Again, that’s not improvement.

And the IEA recently echoed that reality, saying copper projects take far too long to get from discovery to production.

Think about that for a second…

A project being “important” doesn’t mean it’s imminent. And a giant discovery doesn’t mean the market gets metal next year.

Even when companies know where the copper is, they still have to deal with geology, infrastructure, permitting, financing, community relations, water access, processing capacity, environmental rules, and politics.

Then they have to build the thing.

That’s why investors who wait for the supply response to show up in volume often wait much longer than they expected.

This industry deals with one of the longest development cycles in the business world.

Very Little New Supply Has Arrived When You Consider What the World Needs Now

To be fair, copper production has grown over time…

Global copper production has roughly doubled over the last 30 years, to around 22 million tons annually.

But that headline can actually hide the problem…

The issue isn’t whether the world has added any copper. Of course it has.

The issue is whether the industry has added enough large, high-quality, economically durable new supply to match what’s coming next.

And that answer increasingly looks like no.

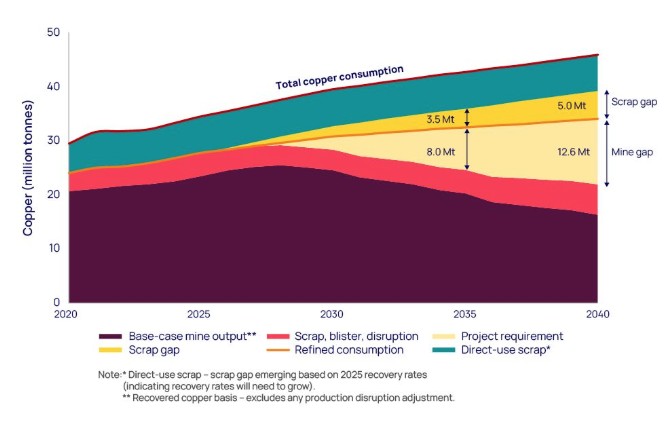

The IEA says that even with announced projects, copper is still headed for a major shortfall by 2035.

S&P Global’s January 2026 work was even more blunt, projecting a copper supply gap of about 10 million metric tons by 2040 if the world stays on its current track.

So yes, some new production has come online over the last 20 years.

But compared with the scale of electrification, grid expansion, industrial rebuilding, and AI infrastructure demand now bearing down on the system, it hasn’t been nearly enough.

That’s the distinction investors need to understand.

This isn’t about “zero growth.” It’s about insufficient growth.

Four Companies Investors Can Use to Play the Trend

If you believe copper is headed into a long-term squeeze, there are a few ways to play it…

Some investors will prefer giant diversified miners with copper growth built in. Others will want more direct exposure.

Freeport-McMoRan is one of the most obvious names to start with.

It remains one of the world’s premier publicly traded copper producers, and its operations give investors major leverage to copper prices.

Freeport reported fourth quarter and full-year 2025 results in January, and in February 2026 it announced an agreement extending operating rights in the Grasberg minerals district for the life of resource.

That’s important because Grasberg is one of the most prolific copper assets on Earth, and long-life assets become even more valuable when replacement supply is scarce.

Southern Copper is another strong candidate for investors who want concentrated exposure.

The company describes itself as one of the largest integrated copper producers in the world. Its 2025 copper production totaled 954,270 tons.

And that kind of scale matters, especially when investors want a real operating business rather than a dream, a PowerPoint, and a drill program in the middle of nowhere.

Southern Copper also has development projects in Mexico and Peru that could help it grow into a tighter market.

Rio Tinto offers a different kind of copper exposure…

It’s more diversified, which lowers the purity of the bet, but it also gives investors a giant balance sheet and meaningful copper growth.

Rio said its 2025 copper production rose 11% year over year, driven by the ramp-up at Oyu Tolgoi, and it has clearly elevated copper as a strategic focus.

That combination of scale, growth, and project depth makes Rio a compelling option for investors who want copper upside without betting the ranch on a single-metal company.

And for investors willing to look a little further down the market-cap ladder, there’s also a tiny sub-$2 company sitting on a copper deposit so large that, by the company’s own framing, it could theoretically supply roughly 8% of global copper demand for the next 40 years, assuming it can finally get the permitting process unlocked.

That’s the kind of asymmetry that makes speculation interesting: a world class resource in a market starving for new supply, paired with the very real political and regulatory roadblocks that have kept it stuck in neutral while copper demand keeps marching higher.

It’s not the low-risk way to play the trend, but if the permitting logjam ever breaks, this hidden gem could go from overlooked to impossible to ignore in a hurry.

Get our new report now to learn more about this under-the-radar copper story and the permitting “loophole” that could send it soaring before the crowd catches on

The Setup Looks Bigger Than a Simple Commodity Trade

What really makes copper especially compelling today is that it doesn’t rely on one macro bet working perfectly…

Copper can benefit if the world goes greener.

It can benefit if the world goes more nationalist and builds more domestic industrial capacity.

It can benefit if AI keeps spreading. It can benefit if grid investment keeps rising.

It can benefit if defense spending remains elevated.

It can even benefit if policymakers panic about supply chains and start throwing money at strategic resource development.

That’s a rare setup.

Usually, one trend drives a commodity story. Copper has half a dozen.

And the supply side still has to deal with a 17-year clock.

The Market May Be Underestimating Just How Tight This Can Get

This is the kind of story investors tend to notice late. Not because it’s hidden, but because it sounds too boring at first.

Copper lacks the glamour that usually attracts fast money. But boring can be beautiful when the fundamentals get tight enough.

Demand is rising from nearly every direction that matters. Discoveries have slowed. New supply takes forever. Announced projects still don’t appear sufficient.

That’s the kind of imbalance that can quietly build for years and then express itself very loudly in prices, margins, and equity valuations.

Copper may not be the sexiest story in the market. But it might be one of the most important.

And when the market finally decides it cares, the best seats may already be taken.

To your wealth,

Jason Williams

@TheReal_JayDubs

@TheReal_JayDubs Angel Research on Youtube

Angel Research on YoutubeAfter graduating Cum Laude in finance and economics, Jason designed and analyzed complex projects for the U.S. Army. He made the jump to the private sector as an investment banking analyst at Morgan Stanley, where he eventually led his own team responsible for billions of dollars in daily trading. Jason left Wall Street to found his own investment office and now shares the strategies he used and the network he built with you. Jason is the founder of Main Street Ventures, a pre-IPO investment newsletter; the founder of Future Giants, a nano cap investing service; and authors The Wealth Advisory income stock newsletter. He is also the managing editor of Wealth Daily. To learn more about Jason, click here.

Want to hear more from Jason? Sign up to receive emails directly from him ranging from market commentaries to opportunities that he has his eye on.

The Best Free Investment You'll Ever Make

We never spam! View our Privacy Policy

After getting your report, you’ll begin receiving the Wealth Daily e-Letter, delivered to your inbox daily.

Angel Publishing Investor Club Discord - Chat Now

Jason Williams Premium

Introductory

Advanced