The Idiot’s Guide to Breaking an Economy

There’s a special kind of policy stupidity that only a central banker can deliver with total confidence.

It happens when energy prices rip higher because supply gets disrupted, trade routes get threatened, production gets pinched, and inflation starts rising for reasons that have absolutely nothing to do with consumers partying too hard or businesses borrowing too much.

In that situation, the right response is to understand the nature of the shock, admit that monetary policy can’t print barrels of oil, and avoid making an already fragile economy even weaker.

Naturally, that’s when the central bankers start reaching for the hammer…

When the Problem Is Supply, Only a Moron Attacks Demand

This is the core point that too many people still miss. A supply shock is not the same thing as an overheated demand boom.

If inflation is coming from consumers spending wildly, wages spiraling, credit exploding, and speculation running hot, then higher rates may cool things off.

But if inflation is coming from an energy shock, broken supply chains, geopolitical violence, or raw material scarcity, then rate hikes don’t fix the actual problem.

They don’t create supply. They don’t reopen shipping lanes. They don’t lower oil production costs. They don’t calm wars.

They just hit demand with a brick and pretend that counts as sophisticated policy.

That’s not monetary genius. That’s vandalism with a Bloomberg terminal.

And if you think that sounds too harsh, I’d argue it’s still too polite.

The Best Free Investment You’ll Ever Make

Join Wealth Daily today for FREE. We’ll keep you on top of all the hottest investment ideas before they hit Wall Street. Become a member today, and get our latest free report: “How to Make Your Fortune in Stocks”

It contains full details on why dividends are an amazing tool for growing your wealth.

The ECB Already Ran This Scam in 2008

We don’t have to speculate about how reckless it is to raise rates into a supply shock, because the European Central Bank already gave us the case study.

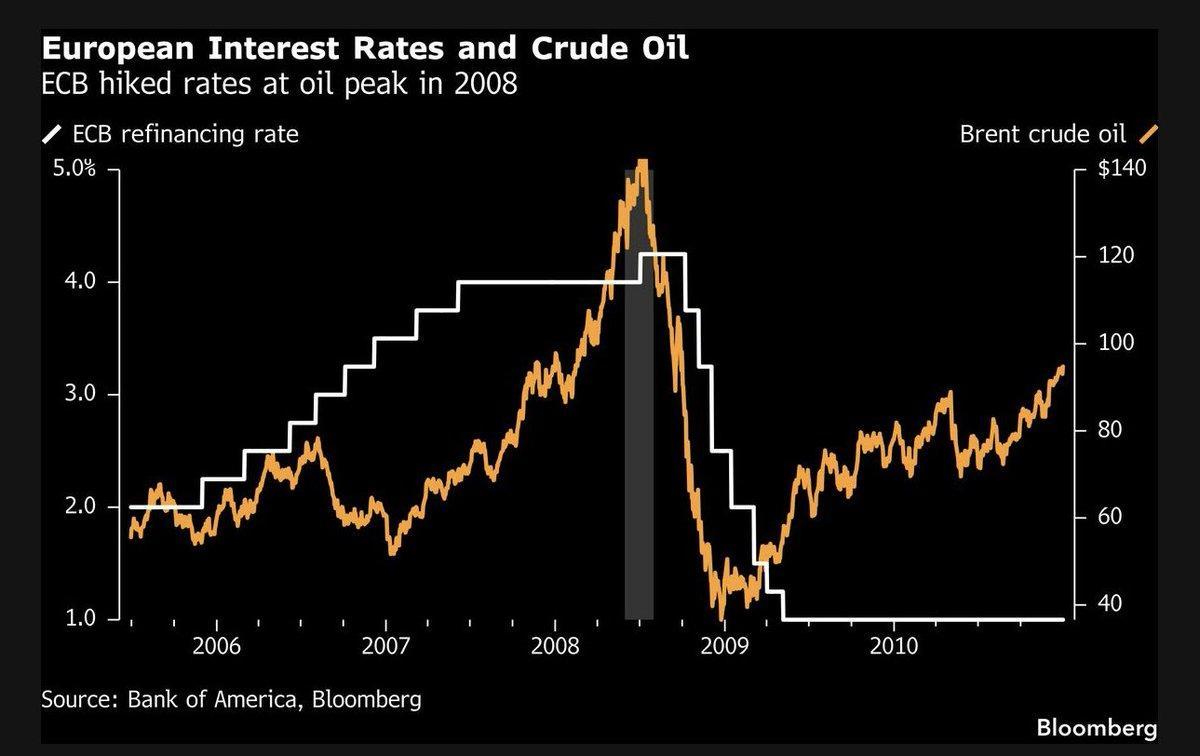

On July 3, 2008, the ECB raised its key interest rates by 25 basis points.

Its official statement said the minimum bid rate on its main refinancing operations would rise to 4.25%, effective July 9, 2008.

The justification was clear enough: Policymakers were worried about inflation and especially about so-called “second-round effects” stemming from higher energy and food prices.

In plain English, they looked at commodity-driven inflation and decided tighter money was the answer.

That should’ve been the moment someone in the room stood up and said, “Gentlemen, this is insane.”

Instead, the ECB did what central banks so often do… It confused visible inflation with inflation it could actually control.

It treated an energy-and-food shock as if it were proof of excessive domestic demand. It tightened policy into weakness and called it credibility.

Then reality punched back…

The ECB’s own 2008 Annual Report lays out the reversal in black and white.

After hiking in July, it ended up cutting rates repeatedly as the economy deteriorated and financial conditions worsened.

And if you zoom out far enough to see the whole arc, the humiliation becomes even more obvious:

From 4.25% in July 2008, the ECB eventually cut its main rate all the way down to 1.00% by May 13, 2009.

That was a total reversal of 325 basis points, or about 77% of the July 2008 target.

That’s the part that matters most. Not merely that they reversed. Not merely that they blinked.

But that they hiked into a shock they fundamentally misread and then had to slash rates by 77% because the economy couldn’t tolerate the stupidity.

That is not a minor policy adjustment. That is an admission of failure on an epic scale.

They Saw Inflation and Forgot to Ask Why

This is where the priesthood of central banking always wants to hide behind jargon.

They’ll say inflation was elevated. True.

They’ll say inflation expectations mattered. Also true.

They’ll say they had to guard against second-round effects. Fine.

But none of that changes the deeper issue, which is that not all inflation is created equal, and pretending otherwise is how you break things.

If energy and food prices surge because the world is experiencing supply disruptions, households get poorer in real time.

Businesses face higher costs. Profit margins get squeezed. Consumers pull back elsewhere. Investment slows. Growth weakens.

That is not a healthy, overheating system that needs to be cooled. It’s a stressed system that is already being taxed by the shock itself.

In June 2008, even before the rate hike, the ECB acknowledged downside risks to growth and noted that further increases in energy and food prices could dampen consumption and investment.

Then, just weeks later, it hiked anyway while still warning about broad-based second-round effects from higher energy and food prices.

That contradiction tells you everything you need to know. They saw the slowdown forming, saw the source of the inflation, and still chose theater over judgment.

That’s what central bankers do when they care more about looking tough than being right.

Pain Does Not Equal Wisdom

One of the most destructive myths in finance is that central banks are full of master technicians carefully calibrating the machine.

Please, spare me…

More often than not, they’re lagging the cycle, misdiagnosing the problem, and then congratulating themselves for responding to the consequences of their own mistakes.

They confuse pain with proof of discipline. They confuse public sternness with actual competence.

They think making things worse in the short term somehow validates the seriousness of their inflation-fighting credentials.

But here’s the rebel truth: If inflation is being driven by a supply shock, higher rates are not medicine. They’re collateral damage.

You don’t solve an oil shock by making mortgages more expensive.

You don’t solve a refinery disruption by crushing credit creation.

You don’t solve a geopolitical energy spike by strangling business investment.

All you do is compound the drag.

The shock hits first. Then the rate hikes amplify it. Then the slowdown gets uglier.

Then the same geniuses who caused part of the damage start cutting rates and acting like heroes for bringing a hose to the fire they helped spread.

That’s exactly what the ECB did in 2008.

It hiked to 4.25% in July. By the following May, it was down to 1.00%.

That 325-basis-point collapse in policy rates wasn’t a sign of nimble brilliance. It was evidence that the original posture had been catastrophically wrong.

The Bureaucrats Will Probably Do It Again Anyway

Now here’s the truly infuriating part…

Even with this history sitting right there in plain sight, I still think the Fed and the ECB are likely to lean in the same direction if the inflation optics get politically uncomfortable enough.

Maybe that means outright hikes. Maybe it means holding rates too high for too long.

Maybe it means jawboning the market with hawkish nonsense about credibility and second-round effects.

The exact flavor of the mistake can vary. The instinct behind it doesn’t.

Because central banks are not nearly as good at their jobs as the market likes to pretend.

Over the past decade alone, they’ve overstayed easy money, fueled asset bubbles, dismissed inflation when it was obvious, and then overcompensated after the fact.

They’ve proven again and again that they’re far better at reacting to stale data than anticipating the real-world consequences of structural shocks.

They’re bureaucracies. They’re designed to move late, speak carefully, and defend themselves endlessly.

That’s pretty much the exact opposite of what you need in a fast-moving supply crisis.

And when this new energy shock reflects in the last month’s inflation data, they’ll be tempted — once again — to treat it like a moral challenge rather than a structural one.

Inflation rises, so they must look resolute. Prices move higher, so they must sound stern. The economy weakens, so they tell themselves the weakness is necessary discipline.

It’s the same old religion, just slightly different robes.

The Real Sequence Is Always the Same

Investors should stop pretending this is mysterious.

First comes the supply shock. Then comes the inflation panic. Then comes the central bank posturing. Then comes the slowdown. Then comes the reversal.

That sequence doesn’t always happen on the same timetable, and the market never moves in a straight line, but the pattern is brutally familiar.

The ECB in 2008 is the perfect example.

It saw higher energy and food inflation, hiked into it, then found itself cutting all the way from 4.25% to 1.00% in less than a year because the economic reality underneath the inflation scare was much weaker than the headline numbers suggested.

And that’s why it would be stupid for the ECB or the Fed to raise rates into a supply shock now. Not controversial. Not edgy. Just stupid.

Historically stupid.

The kind of stupid that comes from mistaking symptoms for causes.

The kind of stupid that punishes the productive economy for a shortage it didn’t create.

The kind of stupid that becomes obvious only after the same policymakers are forced into a frantic U-turn.

Don’t Mistake a Podium for Competence

Contrarian investors need to keep one thing in mind above all else: Official seriousness is not the same thing as intelligence.

A central banker at a podium can sound measured, responsible, and deeply informed while still being dead wrong about the nature of the problem.

We’ve seen it before. We’ll see it again. These institutions don’t magically become competent because the language is polished and the suits are expensive.

If the Fed and the ECB choose to tighten further into a supply-driven inflation pulse, or even if they simply stay too tight for too long because they’re terrified of looking soft, they won’t be solving the shock.

They’ll be deepening the economic damage. And when the damage becomes too obvious to ignore, they’ll cut. They always cut.

The only question is how much wreckage gets created first.

That’s the lesson from 2008.

The ECB hiked to 4.25%, misread the moment, and eventually had to cut to 1.00% by May 2009 — a full 325-basis-point retreat from a policy stance that never should’ve happened in the first place.

So no, it would not be smart for central banks to raise rates into a supply shock.

It would be the kind of dumb decision only an institution with a long record of failure, a short memory, and total faith in its own talking points could make.

Which is exactly why we shouldn’t rule it out.

To your wealth,

Jason Williams

@TheReal_JayDubs

@TheReal_JayDubs Angel Research on Youtube

Angel Research on YoutubeAfter graduating Cum Laude in finance and economics, Jason designed and analyzed complex projects for the U.S. Army. He made the jump to the private sector as an investment banking analyst at Morgan Stanley, where he eventually led his own team responsible for billions of dollars in daily trading. Jason left Wall Street to found his own investment office and now shares the strategies he used and the network he built with you. Jason is the founder of Main Street Ventures, a pre-IPO investment newsletter; the founder of Future Giants, a nano cap investing service; and authors The Wealth Advisory income stock newsletter. He is also the managing editor of Wealth Daily. To learn more about Jason, click here.

Want to hear more from Jason? Sign up to receive emails directly from him ranging from market commentaries to opportunities that he has his eye on.

The Best Free Investment You'll Ever Make

We never spam! View our Privacy Policy

After getting your report, you’ll begin receiving the Wealth Daily e-Letter, delivered to your inbox daily.

Angel Publishing Investor Club Discord - Chat Now

Jason Williams Premium

Introductory

Advanced